UvA economists crack Libor and Euribor scandals as cartels

19 July 2017

Libor and Euribor are important interest rates between banks. In 2008, the Libor and Euribor scandals came to light in which prominent banks were identified as having had manipulated the benchmark inter-bank borrowing rate. Since then, common perception has been that the Libor and Euribor scandals simply involved rogue traders from some of the specified banks who fraudulently manipulated the rates for personal gain, possibly even to the detriment of their own employers. Massive collusion would be too complex to pull off. The US and European authorities indeed treated the cases as fraudulent misreporting in breach of the banking code of conduct and client confidentiality. Only the European Commission prosecuted several panel banks for collusion under the competition rules, Article 101 TFEU.

To date, it is still not known how the cartel operated. Meanwhile, private litigation for cartel damages is progressing slowly, partly because of conceptual questions in the US on whether the Libor and Euribor manipulations could legally be considered under American antitrust law.

Tenacity of benchmark rates cartel

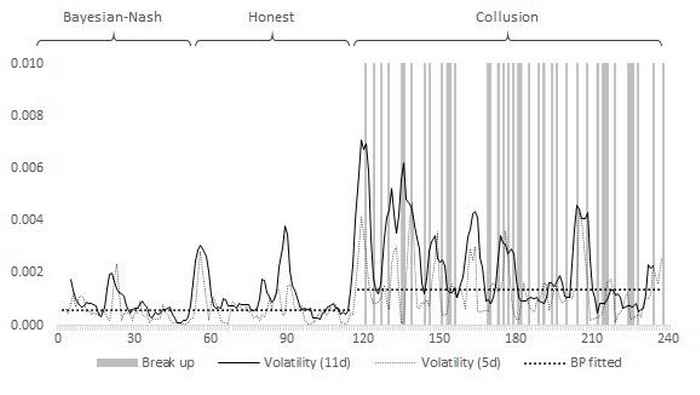

In a new working paper, Nuria Boot (DIW Berlin), Timo Klein (UvA) and Maarten Pieter Schinkel (UvA) show how a continuous benchmark rates cartel could be sustained by pre-emptive portfolio changes using inside information, which would allow the contributing banks to prevent conflicting interests from their trade book positions varying too much. The designated banks can then manipulate certain specific transactions in order to produce the collusive interest rates. Because the cartel is not always able to maintain a stable partnership on account of fluctuating portfolio interests, the members sometimes revert temporarily to non-cooperative behaviour whereby banks (to a certain degree) honestly submit their interest rates.

Vulnerabilities remain

The researchers’ analysis reveals that even after implementation of the proposed reforms of the Libor and Euribor benchmark rate setting processes, which are planned to take effect in the course of 2017, the rates remain vulnerable to collusive manipulation. Periods of heightened volatility in the benchmark rates can be a sign of collusion. ‘This gives us a firm basis for developing new statistical tests with which to detect collusive manipulation’, says Maarten Pieter Schinkel, professor of Economics at the UvA. ‘These methods could in future be used by central banks and other market authorities, or even potential victims (see figure below). Our paper also offers insight into the type and extent of the damages that may have been caused by this kind of cartel.’

Mechanisms also apply to other markets

The cartel mechanisms apply to more recent findings of coordinated manipulation in Foreign Exchange (FX) rates too, as well as to other benchmarks that have recently been subject to allegations of misconduct, including gold, energy and commodities markets.

Publication details

Boot, Nuria, Klein, Timo en Schinkel, Maarten Pieter, ‘Collusive Benchmark Rates Fixing’, Amsterdam Center for Law & Economics Working Paper No. 2017-02, June 27, 2017.